![[Image by creator from ]](/media/images/patrick-lunsford.2e16d0ba.fill-500x500.jpg)

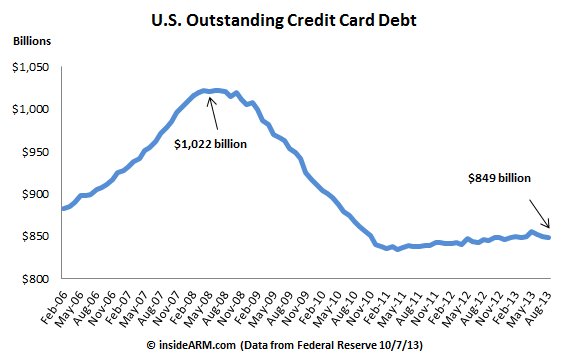

Total consumer credit card debt outstanding fell at an annual rate of 1.2 percent in August for the third straight month, according to the Federal Reserve.

In its monthly consumer credit statistical release (G.19), the Fed said that total balances on credit cards declined by a little more than $1 billion in the month to just under $849 billion. After spiking in May, consumers charged less on their cards over the summer or paid down existing balances.

The decline in August marked the first time in two-and-a-half years that credit card debt outstanding fell in three consecutive months.

Prior to 2011, credit card debt fell precipitously coming off the financial crisis of 2008. The Fed’s G.19 figure for revolving debt fell 25 straight months before finally showing an uptick in March 2011. Since then, growth has been slow but relatively steady over the long run.

Non-revolving debt, meanwhile, grew at an eight percent annual clip in August, driven mostly by auto and student loans.

At the end of August, the Fed noted that total consumer debt outstanding, not including loans backed by real estate, was $3.037 trillion, an all-time high.

![[Image by creator from ]](/media/images/New_site_WPWebinar_covers_800_x_800_px.max-80x80.png)

![[Image by creator from ]](/media/images/Finvi_Tech_Trends_Whitepaper.max-80x80.png)

![[Image by creator from ]](/media/images/Collections_Staffing_Full_Cover_Thumbnail.max-80x80.jpg)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![Webinar graphic reads RA Compliance Corner - Managing the Mental Strain of Compliance 12-4-24 2pm ET [Image by creator from ]](/media/images/12.4.24_RA_Webinar_Landing_Page.max-80x80.png)